Rounds have been up since the pandemic hit and industry analysts are now predicting that it is not just a one-time bump, but a sustaining trend. The swing up has also made golf the fastest-growing sport in the U.S. in terms of overall players, when golf entertainment is included in the mix.

Since June 2020, rounds have only underperformed in two months when compared to pre-pandemic numbers, according to the National Golf Foundation. Those months were April 2022 and 2023, which is largely due to April’s status as the most variable month for golf rounds in the U.S. because of weather. In every other instance, the given month outperformed its pre-pandemic equivalent, some by more than 40 to 60%.

Twenty-four of the past 37 months were higher than their peak equivalent going all the way back to 2007. Only five months in the period ended more than 5% below their 13-year peak, and all of those were months such as February, March, April and November, which already tend to have lower volume because of the weather.

Jim Koppenhaver, an industry consultant from Pellucid Corp. who has long positioned himself as a more pessimistic version of the NGF, said golf has shown surprising resilience in the face of the pandemic.

Jim Koppenhaver, an industry consultant from Pellucid Corp. who has long positioned himself as a more pessimistic version of the NGF, said golf has shown surprising resilience in the face of the pandemic.

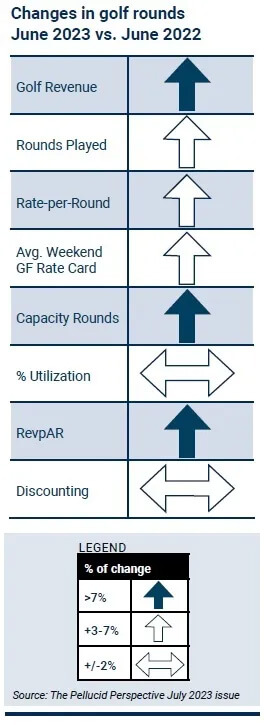

“Looking at the progression of rounds through June versus last year’s results, we’re seeing continued strength in demand against what’s still an elevated base compared to pre-COVID,” Koppenhaver said. “Specifically, five of six months beat 2022 (all but March) and all of them beat the five-year average which is a more ‘normal’ benchmark and includes both pre- and post-pandemic conditions. Our crystal ball for the end of year suggests we could end the year with both record Rounds and Golf Revenue for the post-2000 period for which we have reliable tracking. Has the COVID surge for golf peaked? The current fact-based answer would appear to be, ‘Not yet.’”

As of the beginning of July, the number of rounds played is less than one percentage point behind June 2021’s historic pace, and more than 15% higher than the 2017-2019 average. Off-course golf also continues to grow at a fast pace, introducing golfers to the industry.

In almost any other scenario, these numbers would be cause for celebration. Recent events, however, have made people apprehensive and more than a little hesitant to declare victory.

“Golf’s trajectory is impressive in its own right, but the story is usually modulated for fear of sounding opportunistic … and because the relationship between on- and off-course has been sort of dubious up to this point,” NGF said in August.

NGF noted it is challenging to measure how many golfers off-course golf has produced. But it noted that an estimated 2.5 million of today’s 25.6 million on-course players credit their off-course experiences for getting them to the golf course. And half of on-course participants said off-course “re-engaged them” with golf.

Koppenhaver said weather has also helped bump up numbers, something that could flip the other way in the next year. But, helping the industry is the fact that operators did not increase post-COVID pricing as aggressively as other industries. That has had a positive impact on golfer spending habits and perception. Instead, operators have clamped down on discounts, and consumers have largely accepted that.

So what does that mean for the rest of the year? Both NGF and Pellucid forecast that there’s nothing standing in the way for the trend to continue, barring some unforeseen economic downturn such as a recession.

NGF is perhaps a little cooler than Pellucid — which could be a first in 20 years — noting that online search popularity for golf balls in July fell below the levels from 2022. But that’s a relatively minor trend and shouldn’t detract from the overall message that golf is back.