The numbers speak for themselves.

Since 2019, the year before the COVID pandemic, golf’s largest management companies have experienced unprecedented growth.

Troon has grown from 388.5 to 532 18-hole-equivalent courses. Heiwa Corporation, which owns both Accordia Golf and Pacific Golf Management in Japan, has grown from 313 courses to 379.5. KemperSports has doubled from 102.7 to 206.

In total, the 11 management companies that operate 50 or more courses have grown from 1,164.6 courses in 2019 to 1,796.77 — a remarkable 54% increase that has been driven by post-pandemic demand, record participation and renewed access to capital.

Some of the growth has come through large portfolio acquisitions of third-party management contracts, rather than ownership of the underlying courses. Troon acquired OB Sports in 2019 and Billy Casper Golf in 2021, along with smaller deals. GreatLIFE Golf and Brown Golf Management merged in 2022. KemperSports acquired Touchstone Golf last year.

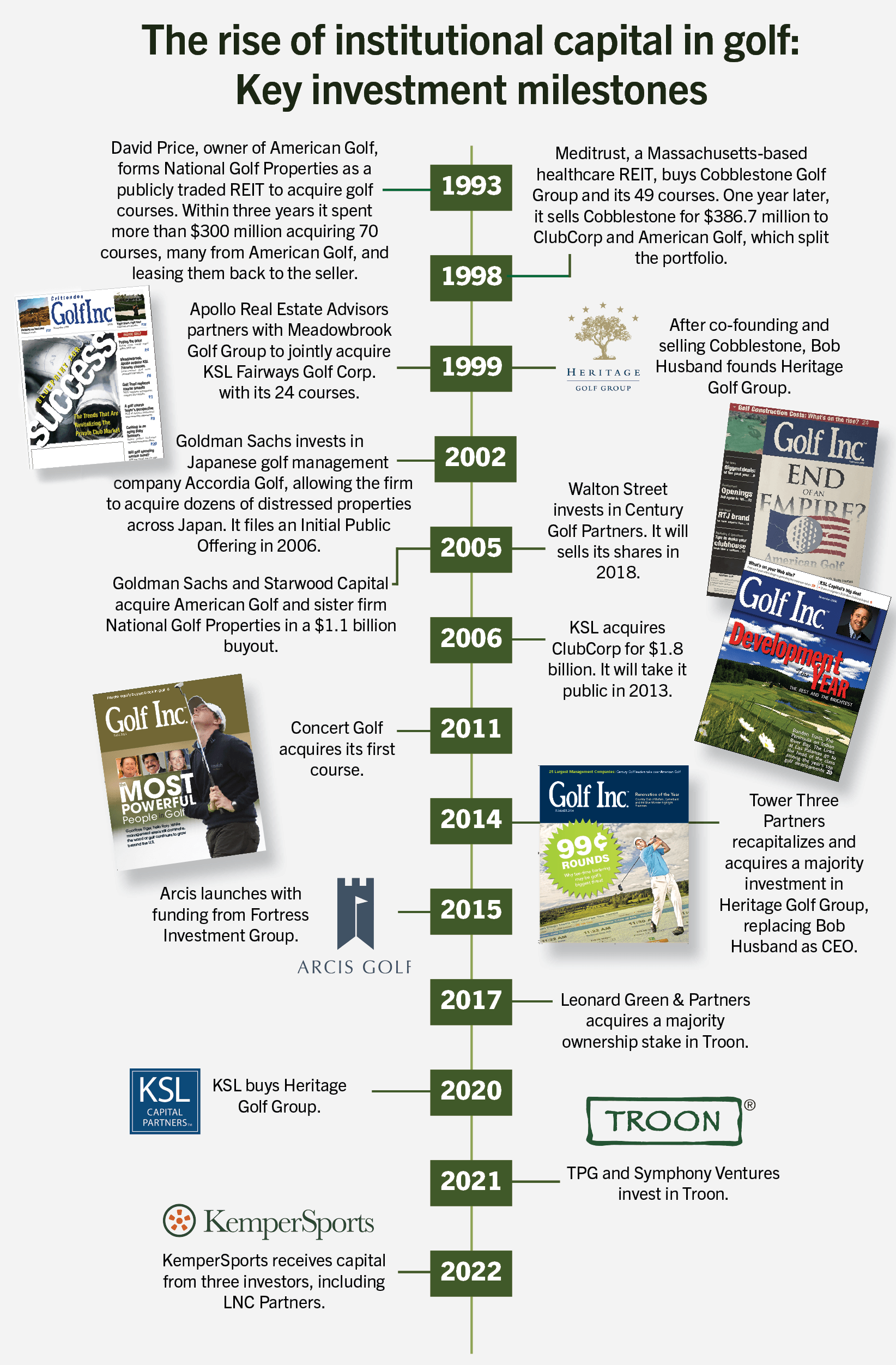

Other companies, including Arcis (26% growth), Century Golf Partners (83% growth), Heritage Golf Group (983% growth) and Concert Golf Partners (275% growth), have expanded primarily through individual course acquisitions.

“I think you will see golf management companies continue to grow, especially some of the smaller companies that want to get big and then exit,” said Chris Karamitsos, senior managing director and partner at Leisure Investment Properties Group, one of the leading brokers in golf. “Eventually private equity will come in and give them a good payday.”

That dynamic is already playing out.

Private equity takes notice

In December, Bain Capital invested in Concert Golf Partners, while KSL Capital Partners acquired Invited — the largest owner of private clubs in North America — in June. In both cases, one private equity firm bought out another.

“Bain’s investment is a great success story,” Karamitsos said. “If you look at how Concert got started and how they grew, it shows what’s possible.”

Peter Nanula founded Concert Golf in 2011 with a clear strategy: acquire underperforming private clubs and invest heavily in improving them. He brought relevant experience: more than 10 years in private equity and seven years leading Arnold Palmer Golf Management from 1993-2000.

After the financial crisis in 2009, distressed golf assets became widely available. Nanula raised capital and targeted struggling private clubs by offering members a compelling pitch: new investment, no assessments and upgraded facilities.

It worked.

Concert grew from zero courses in early 2011 to 20 in 2019, and 50 today.

Bain Capital is the latest institutional investor in the company, following Blackstone Group (2019-22) and Clearlake Capital Group (2022-25).

Nanula said Bain Capital will continue to grow Concert’s platform and invest in its properties.

KSL Capital Partners’ acquisition of Invited tells a similar story about investor confidence in the sector.

It purchased Invited from Apollo Global Management in a transaction valued between $2.6 and $3.0 billion.

“This [acquisition] bodes very well for the golf industry,” said David Pillsbury, CEO of Invited. “KSL knows this company and the business. It should give great confidence that a company this smart and sophisticated has bought the company back.”

KSL previously acquired the company — then known as ClubCorp — in 2006 for $1.8 billion. It took it public in 2013 with a $880 million valuation. Despite generating strong returns, the company faced pressure from activist investors who argued it would be worth more if broken up.

Apollo saved ClubCorp from that fate when it acquired the company in 2017 for an estimated $2.2 billion and took it private again. While initially an aggressive buyer, Apollo shifted its focus in recent years toward improving its balance sheet, selling non-core assets. As a result, its portfolio declined from 212 clubs in 2019 to 161 today — the only major operator on the list to shrink.

That could soon change.

Michael Mohapp, partner at KSL, said the firm plans to work alongside Invited’s leadership.

“We have a deep appreciation for the strength of Invited’s platform and the important role its clubs play in the lives of members and communities,” Mohapp said.

The company is now developing a long-term growth plan that will include acquisitions. Its last deal was Haven Country Club in Boylston, Massachusetts, in September 2022.

“These billion-dollar transactions show there is institutional money and companies that are looking at the golf space,” Karamitsos said. “The yields are very good.”

He noted that golf and other specialty assets have benefited from a commercial real estate market where office, retail and multifamily have delivered weaker returns.

Leisure Investment Properties Group reported in February that it has seen increased participation from traditional commercial real estate investors for the fourth consecutive year, as capital continues to rotate out of multifamily, office, retail and industrial assets in search of higher yields.

Karamitsos said one investor has sold more than 10,000 multifamily units — about one-third of its holdings — and redeployed the capital into golf assets.

“When the three core commercial real estate asset classes come back, it could put downward pressure on golf,” Karamitsos said. “But when interest rates drop a little bit, it will help everything. Investors will be able to come into the golf space with a lot less money.”

Strong fundamentals fuel growth

Golf operators are also benefitting from one of the strongest operating environments in the industry’s history.

Total golf participation has grown 50% during the last decade, now exceeding 48 million golfers, according to the National Golf Foundation. Rounds played reached an all-time high in 2025, the fourth record year in the past five, despite 2,000 fewer courses nationwide. Pellucid also reported that 2025 set multiple modern-era performance records.

That increased play has strengthened operating performance and generated the cash needed for reinvestment — even for companies without significant private equity backing.

Landscapes Golf Management, largely owned by Bill Kubly, has grown from 65 courses in 2019 to 77 today and continues to develop new projects, including Kettle Forge, a new championship golf course located in Ashippun, Wisconsin.

Century Golf Partners, which is owned by its founding executives, including Jim Hinckley and Doug Howe, and investment partners, has grown from 34.5 courses in 2019 to 63.

“Golf is doing so well that if you are not making money, there is something wrong with how you are running your business,” Karamitsos said. “There are three things that golf relies on. You can’t control the weather or the larger economy, but you can control the customer experience.”

Arcis Golf, which has investment from Fortress Investment Group and Atairos, has grown from 70 to 88 courses since 2019, largely by focusing on the membership experience.

The company has invested heavily in renovations, including Cowboys Golf Club in Grapevine, Texas, and the first phase of a $30 million project at the Woodlands Country Club near Houston. It is also pursuing new partnerships, including a new venture with simulator company GOLFZON America.

Among the sector’s fastest-growing operators, however, Heritage Golf stands out.

KSL, the same company that recently acquired Invited, bought Heritage Golf Group in 2020 when it had just six courses. It hired Mark Burnett, the former COO at Invited, to run the company. Since then, the company has grown 983% to 59 courses, primarily through acquisitions.

While sources say the company may slow the pace of expansion, it has already assembled one of the most attractive portfolios in the industry.

If KSL replicates that strategy at Invited, it could redefine the upper limits of scale in private club ownership. Pillsbury, ever the optimist, is ready for the future.

“The best days for Invited are ahead of us and the private club business is exceptional,” Pillsbury said.

This article originally appeared in the July/August 2026 issue of Golf Inc.